[Report by Ouanchao Net, Qi Qian] According to Xinhua News Agency, on July 10th, MP Materials, the largest rare earth producer in the United States, announced that the Pentagon has agreed to acquire its convertible preferred stock for $400 million, thereby becoming its largest shareholder.

The U.S. government aims to promote domestic exploration of minerals and rapid production to break through key mineral bottlenecks and compete with China.

However, several industry insiders in the U.S. expressed on July 25th local time that the aforementioned model may not be replicable. The U.S. possesses rare earth resources but lacks investors willing to take risks in this Chinese-dominated industry. They pointed out that for capital, entering the mining business blindly carries inherent risks.

In recent years, the U.S. has found itself in a dilemma in key mineral sectors: Washington attempts to stimulate the market by investing billions in new mines and processing plants, but due to limited private capital, establishing a domestic rare earth industry remains challenging. Analysts say that the White House’s efforts to break away from dependence on China’s key minerals reveal the U.S.’s vulnerabilities.

It is common for such paradoxes to exist among small companies attempting to extract rare earth elements. U.S.-related companies’ stocks are often traded on smaller exchanges in Canada or Australia, and major banks are cautious about projects that might take ten years or even longer to realize.

According to reports, in January this year, American Rare Earths, an Australian company listed on the Australian Stock Exchange, announced that its wholly-owned enterprise Wyoming Rare Earths had obtained permission to test the “Cowboy State Mine” project at Hollick Creek.

However, U.S. rare earth companies are known for their low-priced stocks.

“Finance is a big issue,” said Joe Eaves, president of the Wyoming project at the company. He believes that the U.S.’s rare earth market “has hardly developed” due to China’s dominant position in the rare earth sector.

The report mentions that commodities like oil have mature financial markets where businesses and traders can hedge against fluctuations, and prices also help investors assess a company’s value and banks design loans. However, the rare earth market is not like this. Seventeen rare earth elements are indispensable for the high-tech industry despite their small demand.

According to data from the International Energy Agency, China accounted for over 60% of the global rare earth mineral output in 2023. However, its control over the processing stage accounts for 92% of the global output, virtually monopolizing the rare earth processing field worldwide. The U.S. Geological Survey also stated that from 2020 to 2023, 70% of the imports of rare earth compounds and metals from the United States came from China.

Earlier this year, China implemented export controls on rare earths, leading American companies such as Ford to seek alternative suppliers. The U.S. views this move as an increase in China’s bargaining power in the Sino-U.S. trade game. Despite some relaxation of restrictions, data shows that China exported 3,188 tons of rare earth magnets to the world in June, down 38.1% compared to the same period in 2024.

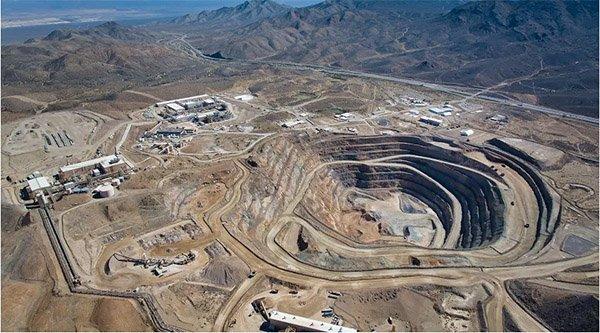

MP Materials’ rare earth mining and processing facilities in Mentor, California

To reduce dependence on China, the U.S. Department of Defense made a rare investment of $400 million in July, becoming the largest shareholder in Mentor Mining, the largest U.S. rare earth producer. Mentor Mining is the only U.S. company to have complete control over the entire rare earth industry chain and is the only one in North America to engage in large-scale mining and processing of rare earth ores. The company owns the world’s second-largest rare earth mine in California, Mentor Mountain.

These measures have triggered dramatic fluctuations in the stock prices of similar companies, which have begun to compete for government funding under the banner of “Made in America.” American miners are hopeful that the federal government can stimulate investor enthusiasm.

In a week, the stock price of an American rare earth company nearly doubled, reaching $46 per share. The company plans to build a “Cowboy State Mine,” which is expected to expedite the permitting process. This mine will contain the “four major core” rare earth elements needed to manufacture strong permanent magnets: Nd, Praseodymium, Dysprosium, and Terbium. However, the CEO of the company had just resigned not long ago, marking the second high-level change in the past year.

“The government has realized that this game isn’t working,” said Randal Atkins, CEO of Ramaco Resources, a Kentucky coal producer. The company recently opened a coal and rare earth mining operation in Wyoming.

Analysts believe that relying on government assistance carries risks, as the United States’ policies on key minerals are long-term inconsistent. For example, the Inflation Reduction Act introduced during the Biden administration includes a domestic production tax credit, but the Trump administration announced these credits would end starting from 2030.

Milo McBride, a researcher at the Carnegie Endowment for International Peace, stated that reducing other credits for electric vehicle purchases and renewable energy development by the U.S. government “poses a risk of扼杀需求 signals, making it impossible to ensure these emerging industries (mostly startups) have access to the market.”

As for whether the transaction involving Manitou Pass Materials could be replicated with other rare earth miners, the Pentagon has yet to provide a clear response.

Some analysts caution that entering the mining business blindly carries inherent risks, with some projects being speculative. Previously, a cobalt mine in Idaho, after thirty years of development despite receiving hundreds of millions of government support, remained dormant for many years.

Rod Egget, an economics professor at Colorado School of Mines, stated, “For these projects, (commercial production) may seem uncertain, but that’s the essence of the industry.”

It is worth mentioning that since China introduced new regulations on rare earth control, the United States, Australia, India, and several Western companies have accelerated their investment in key minerals, attempting to diversify the rare earth supply chain. However, analysts point out that China has accumulated years of expertise in rare earth processing capabilities and talent reserves, making it difficult for other countries to easily “end” China’s dominant position.

Cameron Johnson, a senior partner at TidalWave, a consultancy based in Shanghai, and former vice president of the Shanghai American Chamber of Commerce, anticipates that the diversification strategy of rare earth supply for other countries will face numerous severe challenges, including time, cost, and human capital.

“The time required alone could be at least 10 to 20 years, with costs amounting to trillions of dollars,” said Johnson. “And where do we get the talent? Who knows how to process these materials? Who understands purification processes? How can we achieve high purity? Talent is not available in most countries.”