Cailian Press, August 2nd (Editor: Xiaoxiang)

In the investment world, there’s often a playful jest about “Goldman Sachs buying back, and villas by the sea.” Although this is often just a joke in many cases, this week’s historic plunge in the New York futures copper market still put Goldman Sachs’ sales team in an awkward position—because just the day before this plunge, Goldman’s salespeople had recommended clients to go long on copper…

According to insiders, during a phone conference with clients on Tuesday, Goldman believed that Trump would likely impose a 50% copper tariff and suggested buying short-term bullish options on New York copper, expecting these options to be profitable if New York copper soared by 11%.

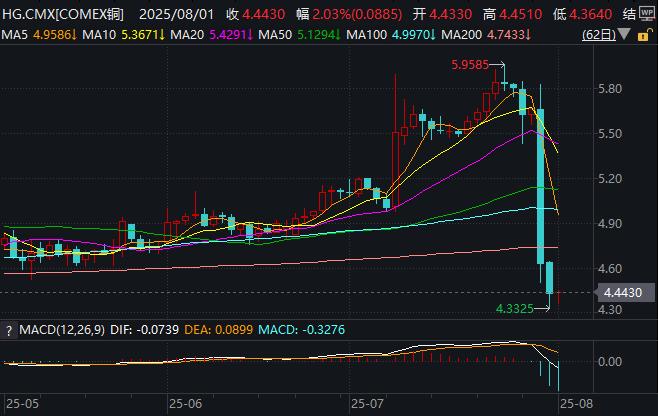

However, in reality, President Trump only imposed limited tariffs on Wednesday afternoon local time and completely exempted major commodity trading forms of copper (such as copper ore, concentrate, galvanized copper, cathode copper, and anode copper), causing New York copper prices to plummet by 22% within just a few hours.

That evening, Goldman’s commodities sales department had to send out an email titled “We are wrong for not paying the copper tariff” to clients.

Undoubtedly, this mistake in copper price forecasting by one of the world’s most prestigious investment banks highlights how Trump’s tariff announcement nearly caught the entire copper market off guard.

Insiders mentioned that several hedge funds and bank trading departments, including Goldman, suffered losses due to the sharp drop in New York copper prices on Wednesday—this decline was twice the largest recorded historically since 1988.

Some other large banks might have also misjudged at that time. It is reported that Citigroup’s salespeople also sent out information to clients on Wednesday morning stating, “Our trading department likes to engage in copper arbitrage trades (buying COMEX, selling LME).

Before the “bullish” stance on Tuesday, Goldman Sachs had been recommending clients to bet on an increase in U.S. copper prices.

Trump initially announced in early July that copper tariffs would be raised to 50%—twice as much as market expectations at the time, but the price of Comex futures copper only rose by about 28% above global benchmark LME copper prices—theoretically, this premium should have approached the 50% set by the tariffs.

Despite some clients’ concerns over potential tariff exemptions for specific countries following the signing of trade agreements with major copper-producing countries like Indonesia, Goldman Sachs still insisted that the price spread between the two markets would continue to widen.

In a summary sent to clients during the Tuesday phone meeting, Goldman Sachs pointed out that “full implementation of a 50% tariff” would expand the COMEX-LME spread to 35%-40%.

As a result, Goldman Sachs recommended clients to buy call options on New York copper with a strike price of $6.25 and a September expiration—about 11% higher than the current market price.

However, as Trump’s copper tariff announcement was made and followed by a sharp drop in New York copper prices, the value of these options had already depreciated by more than 90%…

Interestingly, the content of the telephone and email advice provided by the sales team at Goldman Sachs was contrary to the report released by the research team.

Although the metal analysts at Goldman Sachs had also predicted a 50% tariff on copper, they believed in Monday’s report that “mineral diplomacy” could lead to tariff exemptions and suggested profit-taking from previously recommended positions on the Comex-LME spread.